South East hopes for tourism boom but fears border headache post Brexit

Written by: Nick Phipps

5 June 2017

Brexit could lead to a boom in tourism and high-end exports in the South East, according to a consultation of locals by trade experts at the University of Sussex.

However, there is growing concern about the logistical headache of potentially increased customs and immigration checks at South-East airports, seaports and the Channel Tunnel, the process found.

With the UK General Election only a week away, and with Brexit such an important issue for this election campaign, economists and lawyers from the UK Trade Policy Observatory (UKTPO) based at the University of Sussex have been exploring the key issues for post-Brexit trade policy for the South-East region.

Through consultation with government departments, local businesses and civil society organisations, UKTPO enabled members of the local population to identify the key challenges and opportunities for trade for the South East region as a result of Brexit.

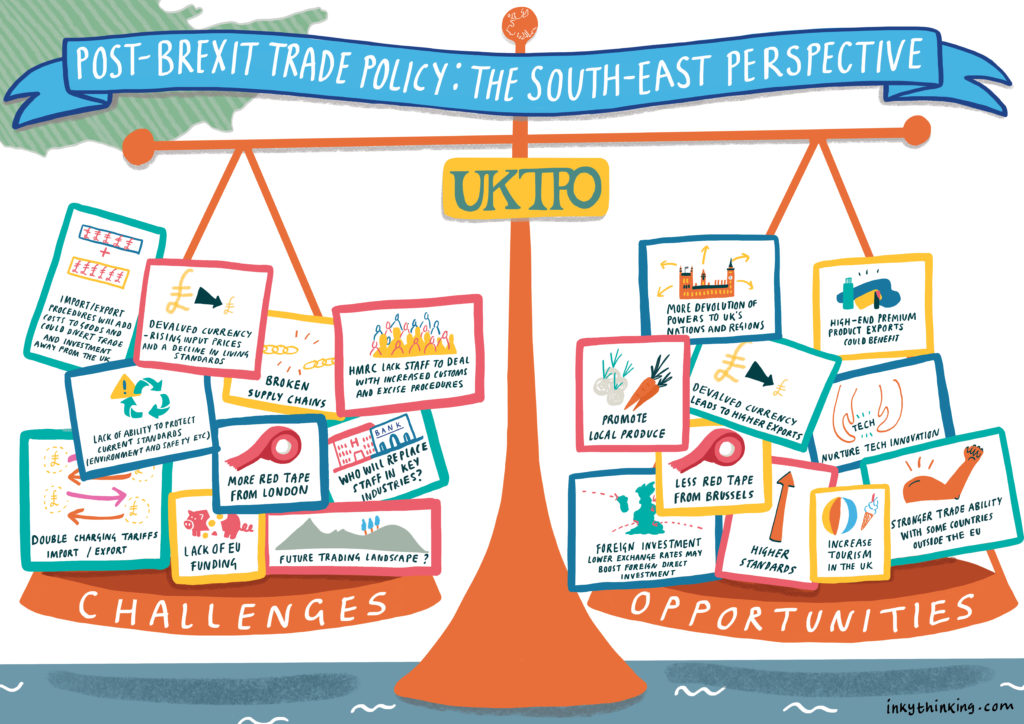

Presented in an illustrative graphic, the key challenges relate to the services and logistics industries which are both important sectors for the region, whilst key local opportunities include tourism. Yet many of the issues raised are of relevance for all UK nations and regions – for example, import and export procedures adding costs to goods and diverting trade away from the UK, and the potential of high-end premium products to benefit from new export opportunities.

Impact

South East England one of the UK’s most successful regions. According to the Office for National Statistics, gross disposable income per person is £20,434, second highest after London (the national average income per head is £17,965). This income is not generated by a large manufacturing sector but by an extensive services sector.

According to the Office for National Statistics, the South East has around 38,000 people employed in the financial sector, and the region would be directly exposed to potential job losses resulting from banks and insurers relocating to EU member states to retain market access.

However, Brexit will have another (indirect) impact on many service suppliers in the South East: many services ‘piggyback’ on manufacturing and agriculture, so any serious loss of EU market access for manufacturing, even for firms elsewhere in the country, would have a significant impact on the demand for services from the South East.

One of the biggest effects that will be seen in the region, given its importance as a gateway, will be the impact on logistics. All of its airports, seaports and the Channel Tunnel will now have to consider how they will deal with UK customs controls as well as immigration. Seaports and airports will need to expand inspection facilities for goods like meat and vegetables. This will require investment in people (which highlights a potential positive impact in terms of employment) as well as new facilities.

Professor L. Alan Winters, Director of UKTPO said

“Consultation is a key ingredient in the formulation of good policy. From our conversations with people in our local area, we were able to understand how future policies would impact on key sectors of our local economy as well as nationally. In order to ensure that new trade policies are constructed in a manner that benefits all, it is important that policy makers engage with and listen to society.”

Analyses

Challenges

Import / Export procedures will add cost to goods and could divert trade and investment away from the UK

Britain is currently part of the same ‘customs territory’ as the rest of the EU and so trade is subject to very few border (customs) formalities (just as trading between Surrey and Sussex is). Even if we sign a free trade agreement that eliminates tariffs and differences in standards with the EU, there will still be customs formalities on EU-UK trade – paperwork, inspections and occasional delays and uncertainty as a result. These increased costs discourage trade and this, in turn, might make investing in Britain less attractive.

Devalued currency – rising input prices and a decline in living standards

When sterling falls, foreign goods and services cost more in terms of pounds. This affects both inputs into UK production and consumers’ purchase of foreign goods and services. In the latter case, if wages don’t keep up, our money doesn’t go as far and we are worse off.

HMRC lack staff to deal with increased customs and excise procedures

Extra customs formalities will raise costs under any circumstances, but particularly if there are insufficient staff to manage them effectively.

Lack of ability to protect current standards (Environment and safety)

Many environmental and safety standards derive from EU regulations. In their absence, the UK government might decide to aim for lower standards, especially if it came to a trade-off between lower standards and access to markets in countries with which it was negotiating trade agreements.

More red tape from London

Many EU regulations will be replaced by UK regulations covering the same areas. These may or may not be more burdensome. Many of the regulations that UK business finds burdensome – e.g. minimum wages and planning law – are homegrown.

Double charging tariffs import / export

Many goods cross the EU-UK border several times in the course of production. If tariffs are introduced on such trade (the so-called ‘no deal’ scenario) they might have tariffs levied on them at each crossing. One can devise ways of avoiding this, but at the expense of the bureaucratic costs entailed in keeping track of the various components so that tariffs can be levied at the end of the process.

Lack of EU funding

The EU funds elements of a number of activities directly including agriculture and research. Brexit will remove this source of funds and its replacement will be a matter of discretion for the UK government.

Future trading landscape?

It is not clear yet whether the UK will have a deep and comprehensive trade agreement with the EU, none at all, or somewhere in-between. Similarly, it is not yet determined what tariffs the UK will levy on trade from non-EU countries and what sort of trade agreements (if any) will be signed with them. All this uncertainty is bad for business and investment.

Opportunities

More devolution of powers to the UK’s nations and regions

Some areas of policy that are currently run by the EU – e.g. agricultural and fisheries policies – will pass to the devolved national administrations. Moreover, some commentators have argued that Brexit provides an opportunity to devolve further powers to the nations and to the English regions.

High-end premium product exports could benefit

Brexit is likely to reduce existing UK exports to the EU, so in order to keep importing, the UK will need to find new products and markets. Since its comparative advantage lies in relatively sophisticated goods and services, these are likely to be the more successful sectors in increasing foreign sales.

Promote local produce

If the costs of importing increase, some buyers will switch their demand to local producers.

Devalued currency leads to higher exports

When sterling falls, a given price in pounds translates into a lower price in dollars or any other foreign currency. This will tend to boost sales, at least to some extent.

Nurture tech innovation

Brexit will be a shock and shocks can stimulate innovation and fresh thinking. This is especially so for exporting sectors because the devaluation of sterling and other pressures to increase exports will increase the returns on innovation in those sectors.

Foreign Investment – lower exchange rates may boost foreign direct investment

If you are outside the UK and want to buy a British firm whose value is given in terms of sterling, you need fewer dollars to do so. At least in the short run, there are probably some bargains to be had.

Higher standards

EU standards reflect average views and opinions across the whole EU. After Brexit, they need reflect only average UK views and in some cases (e.g. animal welfare) these may be to seek higher standards.

Increase tourism in the UK

With a weaker (devalued) pound, it is cheaper in terms of Euro or other foreign currencies to visit the UK.

Stronger trade ability with some countries outside the EU

At present, the EU negotiates trade agreements as a bloc and so the outcome reflects the wishes of all EU members. When the UK negotiates alone, it may have less negotiating power (because its market is much smaller than the EU’s), but it can all be focussed on UK objectives. An example: the EU currently has a tariff of over 16% on oranges when Mediterranean producers pick their crops, but this serves no UK goal.

Notes

Local consultation process

Last month UKTPO held a public event in Brighton to discuss ‘What are the priorities for Britain’s Trade Policy Post Brexit?’ The event included a World Café session that enabled participants to discuss the trade issues they believe are important with each other and with UKTPO’s experts. The data will help inform the future work of the Observatory, and UKTPO fellows can also feedback to policy makers, providing the opportunity for more inclusive trade policy-making.

All the information in this blog is available in a leaflet: Post Brexit Trade Policy: The South East Perspective

Disclaimer:

The opinions expressed in this blog do not necessarily represent the opinions of the University of Sussex or the UK Trade Policy Observatory.

Republishing guidelines

The UK Trade Policy Observatory believes in the free flow of information and encourages readers to cite our materials, providing due acknowledgement. For online use, this should be a link to he original resource on the our website. We do not however, publish under a Creative Commons license. This means you CANNOT republish our articles online or in print for free.